From: Williams, Carter <carter@oiventures.com>

Sent: Wednesday, December 10, 2025 1:13 PM

To: Tom Graham <tom@grahamre.com>; kathy.motschall@yahoo.com; Jamielynnmelke@gmail.com; Reeve 4 HS Council <wendy@reeve4hscouncil.com>; Jeanne Benjamin, <jjmb1011@yahoo.com>

Cc: Victor Sinadinoski <citymgr@cityofharborsprings.com>; Kyle Knight <KKnight@cityofharborsprings.com>; NW Whitaker <cityclerk@cityofharborsprings.com>

Subject: 2026 Budget

Mayor Graham and City Council,

I had a moment to listen to Monday’s budget discussion. I had a few thoughts on changes we should make to the budget. I am sharing with you my review of the proposed FY2026 budget and CIP. The analysis is offered constructively. The goal is a budget that balances without relying on uncertain revenues and provides clearer accountability for major commitments like the electric utility bond and DDA spending. While you are likely not required to follow GAAP, it’s a good practice.

The analysis identifies several areas where tighter alignment with GAAP principles and clearer strategic guidance would benefit the City. The core recommendations are straightforward:

Balance the budget without relying on uncertain FEMA revenue

2. Remove unfunded projects from the operating budget; keep them in the CIP as contingent

3. Require a 10-year pro forma before finalizing the electric utility bond

4. Establish measurable KPIs for the DDA before approving their budget

5. Invest in citizen communications infrastructure to reach 90%+ of property owners and voters

Happy to discuss any questions,

Respectfully,

Note: Please include in CC packet for the next meeting.

Click on this LINK to download letter in entirety HS 2026 Budget Analysis

CITIZEN BUDGET REVIEW BY CARTER WILLIAMS 12.10.25

City of Harbor Springs, Michigan

Fiscal Year 2026 Proposed Budget

December 2025

Purpose and Limitations

This memo is offered in the spirit of a citizen management letter—highlighting areas where

closer alignment with Generally Accepted Accounting Principles (GAAP) and government

finance best practices could strengthen the City’s budget presentation and fiscal planning.

Important Disclaimer: This review was conducted with limited time and access to

underlying documentation. I may have missed context, corrections, or explanations that

would address the observations below. Staff and Council are far more familiar with the

details than I am, and I welcome correction on any point where I have misunderstood the

situation.

The intent is not to criticize staff effort—preparing a budget for a city with this level of

complexity (municipal electric utility, DDA, waterfront, capital plan) is substantial work.

Rather, this memo suggests ways to strengthen governance and transparency that would

benefit any municipality of our size.

Context: Harbor Springs has a year-round population of approximately 1,200 residents, with

significant seasonal fluctuation. The City operates its own electric utility, maintains waterfront

facilities, and supports a tourism-oriented downtown through a Downtown Development

Authority (DDA).

Summary

Based on my review of the proposed FY2026 budget and the December 8, 2025 Council

discussion, I identified several areas where GAAP best practices suggest modifications.

These relate primarily to revenue recognition, capital project authorization, liability accrual,

and enterprise fund oversight.

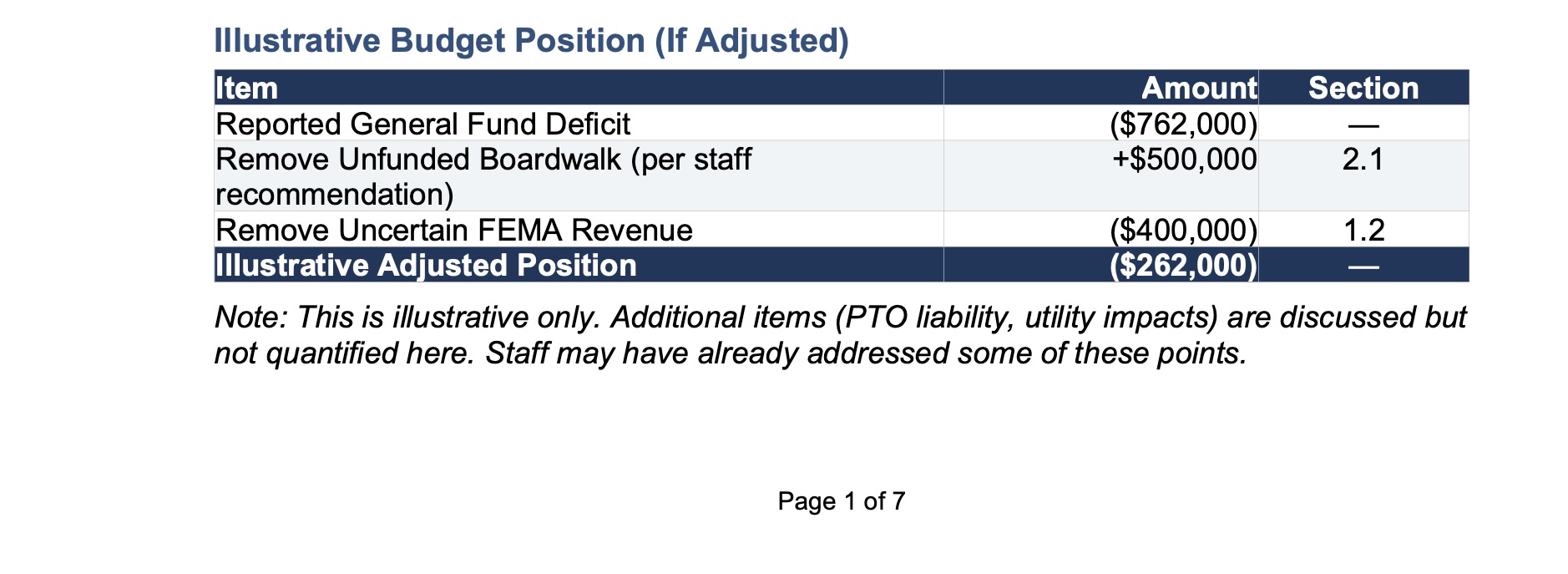

The budget as presented shows a General Fund deficit of $762,000. However, this figure

includes a $500,000 boardwalk project that staff recommends removing, and $400,000 in

FEMA revenue whose timing and amount remain uncertain. Adjusting for these items would

significantly change the reported position.

The recommendations below are offered as suggestions for Council’s consideration,

grounded in GAAP principles and best practices from the Government Finance Officers

Association (GFOA).

Illustrative Budget Position (If Adjusted)

Section 1: GAAP Best Practices – Revenue and Liability

Recognition

GAAP and GFOA best practices provide a framework for consistent, conservative financial

reporting. The following observations highlight areas where closer alignment with these

standards could strengthen the budget presentation.

1.1 Accrual of Compensated Absences (PTO)

GAAP Standard: GASB Statement No. 16 requires governments to accrue a liability for

compensated absences (vacation, sick leave, PTO) that are attributable to services already

rendered and are not contingent on a specific event.

Best Practice Rationale: Accruing these liabilities annually ensures that current taxpayers

fund the benefits earned by current employees, rather than creating budget surprises when

long-tenured employees retire.

Observation from December 8 Meeting:

• Discussion indicated that a retiring officer’s PTO payout plus healthcare buyout

totaled approximately $160,500

• Staff noted that PTO can accumulate up to six months and payout percentages vary

by tenure

• This suggests the City may be using cash-basis recognition for these obligations

Suggestions for Consideration:

1. Calculate and disclose total accumulated PTO liability across all funds

2. Consider establishing an Employee Benefit Reserve Fund with annual contributions

3. Publish an annual schedule showing total liability and year-over-year changes

1.2 Recognition of Contingent Grant Revenue (FEMA)

GAAP Standard: GASB Statement No. 33 requires that grant revenue be recognized only

when eligibility requirements are met and resources are measurable and available. Until a

grant is formally awarded and funds obligated, the revenue is considered a contingent asset.

Best Practice Rationale: Conservative revenue recognition protects against budget

shortfalls if expected grants are delayed or denied. This is particularly important for FEMA

reimbursements, which can take months or years to process.

Observation:

• The budget includes $400,000 in anticipated FEMA reimbursement (approximately

9% of General Fund revenue)

• Staff indicated uncertainty about timing: “That could be 10 days, it could be two

years”

• Some permanent work claims have already been denied

• Grant is currently in “final signature in review” with State Emergency Management

Suggestions for Consideration:

1. Consider presenting a base budget that balances without FEMA revenue

2. Identify specific projects or reserve replenishment that would be funded if FEMA is

received

3. Consider adopting a policy that FEMA funds first replenish reserves drawn down for

storm response

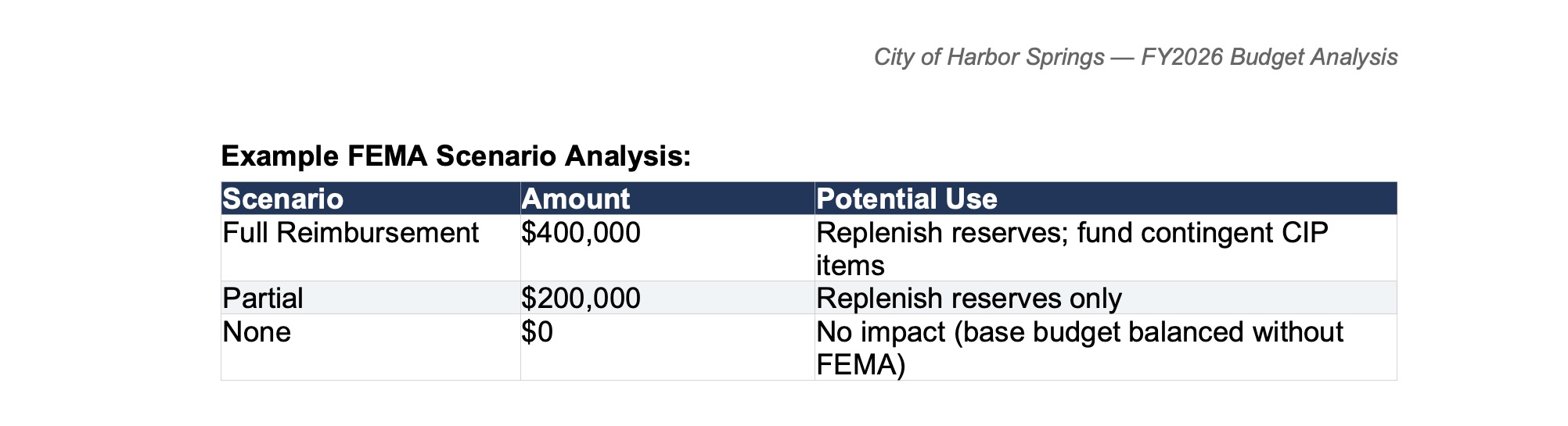

4. Present scenario analysis (full/partial/no FEMA) to help Council and citizens

understand the range of outcomes

Page 2 of 7City of Harbor Springs — FY2026 Budget Analysis BY CARTER WILLIAMS

Section 2: Capital Improvement Plan Structure and Transparency

GFOA best practices recommend that capital budgets clearly distinguish between funded

and unfunded projects, and that aspirational projects not be included in appropriations until

funding is secured.

2.1 Contingent Projects in the Operating Budget

Best Practice: Capital projects that depend on external funding (grants, donations) should

not appear as appropriations in the annual operating budget until funding is contractually

committed. Including them creates a misleading deficit narrative.

Observation:

• The budget includes a $500,000 boardwalk project without corresponding revenue

• Staff recommended removing this item: “We’re not showing any revenue coming in

donations in 2026″

• City Manager stated: “My recommendation there is to remove the boardwalk from

this budget”

Suggestion: Follow staff’s recommendation to remove the $500,000 boardwalk expenditure

from the operating budget. Keep it in the CIP as a contingent project to be initiated when

sufficient donations and/or grants are secured. Post the CIP on City website along with

budget. If there are important unfunded elements, include the logic/concern/outreach for

funds via city newsletter/facebook/website.

2.2 Restricted Fund Reconciliation

Best Practice: Restricted funds should be fully reconciled before authorizing new spending,

with clear documentation of receipts, expenditures, and current balance.

Observation:

• There appears to be some uncertainty about the current boardwalk fund balance (Not

sure I have this right, it was hard to distinguish in the transcript)

• Historical audit records and current reported balances may warrant reconciliation

Suggestion: Before any future boardwalk spending is authorized, consider presenting a

complete reconciliation showing: total donations received by year, expenditures to date,

current restricted balance, and any transfers or reclassifications.

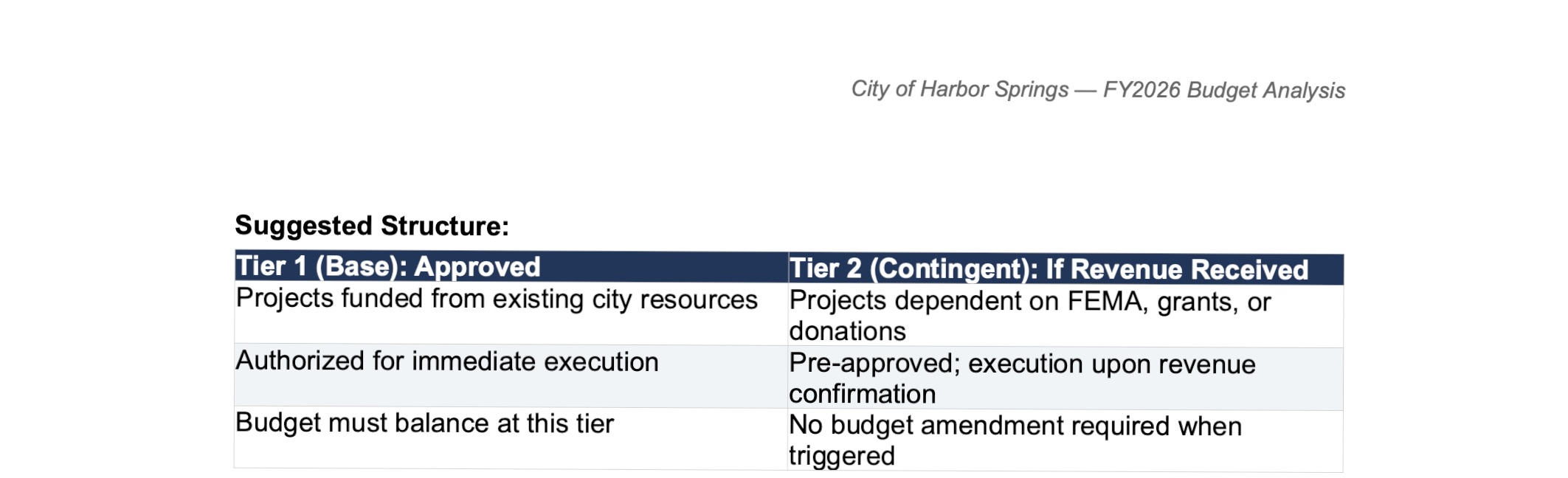

2.3 Tiered CIP Approach

Best Practice: GFOA recommends that capital plans clearly distinguish between projects

that are funded and ready for execution versus those that are contingent on future

resources.

Page 3 of 7 City of Harbor Springs — FY2026 Budget Analysis BY CARTER WILLIAMS

Suggested Structure:

Benefit: This approach maintains fiscal discipline while allowing rapid execution of deferred

projects when revenue materializes, without requiring a budget amendment. Post a memo

explaining the tiered approach on city website

2.4 CIP Publication and Strategic Guidance

Best Practice: GFOA recommends publishing the full CIP alongside the annual budget, with

clear status indicators for each project.

Suggestions:

1. Publish the CIP on the City website with projects clearly labeled as Funded,

Contingent, or Unfunded

2. For unfunded items, include estimated cost and anticipated funding sources

3. Consider providing Council guidance on strategic priorities (e.g., relative emphasis

on resident infrastructure vs. tourism amenities) to help staff rank and sequence

projects consistently

Benefit: Transparency allows citizens to see not just what the City can afford this year, but

what it aspires to do over time. Residents can provide informed input on priorities.

Section 3: Electric Utility Fund Oversight and Reporting

The proposed $8 million utility bond authorization represents a significant commitment for a

city of 1,200 year-round residents. GFOA best practices suggest that enterprise fund

borrowing of this magnitude warrants detailed analysis and enhanced oversight.

3.1 Bond Sizing and Debt Service Planning

Observation:

• $8 million authorized, though final engineering is not complete

• Staff indicated a preference to bond for $6 million if possible

• The method for funding debt service (rate increases vs. General Fund support)

appears undetermined

• Council discussed eliminating the $245,000 annual Electric Fund transfer to General

Fund

Suggestion: 10-Year Pro Forma

Before finalizing bond size and rate decisions, consider presenting a 10-year Electric Fund

pro forma including:

1. Forecasted operating revenues and expenses

2. Planned capital expenditures beyond current projects

3. Proposed bond structure and debt service schedule

4. Planned transfers to General Fund (if any)

5. Projected debt service coverage ratios

Page 4 of 7City of Harbor Springs — FY2026 Budget Analysis

6. Target minimum fund balance and reserve requirements

3.2 Transfer Policy

Best Practice: Transfers from enterprise funds to the General Fund should be based on a

clear, documented policy rather than ad hoc decisions. The policy should include safeguards

to protect utility financial health. Policy should be posted on city website.

Suggestion:

• Consider formalizing the transfer policy with a defined formula (e.g., percentage of

revenues or net plant)

• Include automatic safeguards: if debt service coverage or fund reserves fall below

target thresholds, transfers are reduced or suspended

• Document the General Fund impact under different transfer scenarios

3.3 Emerging Risks and Oversight

Observation:

• The City recently sold a Power Purchase Agreement, suggesting active capacity

management

• Seasonal population fluctuation (1,200 to potentially 5,000+) creates variable peak

demand

• Regional trends toward electrification (heat pumps, EVs) may increase future load

and increased supply of renewables may make supply intermittent.

• There does not appear to be regular, formal utility reporting to Council beyond budget

documents. Council is running a utility, and needs to oversee it properly.

Suggestions:

1. Quarterly Reporting: Consider establishing quarterly or semi-annual Electric Fund

reports to Council covering demand trends, capacity utilization, project status, and

fund balance

2. Advisory Input: Given the complexity of utility operations, consider engaging an

informal advisor, perhaps a retired utility executive residing in the community, to

review the bond business case, load assumptions, and rate impact before debt is

incurred

3. Load Analysis: Survey community on the rate at which it is moving more electric.

And/Or discuss with HVAC contractors. The shift to more electric was a reason for

the multi-day winter blackout in Texas.

Section 4: DDA Accountability Framework

The Downtown Development Authority spends approximately $270,000 annually, funded

largely by TIF capture (~$181,000) and special assessments. GFOA best practices suggest

that entities receiving dedicated tax revenue should demonstrate measurable outcomes.

4.1 Performance Measurement

Best Practice: Organizations funded by dedicated revenue streams should establish Key

Performance Indicators (KPIs) that connect spending to outcomes, allowing stakeholders to

evaluate return on investment.

Observation:

• The DDA budget presentation focused on activities (events, beautification,

marketing) rather than outcomes

Page 5 of 7 City of Harbor Springs — FY2026 Budget Analysis BY CARTER WILLIAMS

• No KPIs were presented to measure effectiveness

• Fund balance is approximately $430,000 (growing) with no stated deployment plan

Suggestion:

Before approving the FY2026 DDA budget, Council might ask the DDA to propose a small

set of KPIs and provide a good-faith estimate of current performance against those metrics.

This need not be onerous—even simple measures like commercial vacancy rate, year-round

vs. seasonal business count, or taxable value growth would provide baseline accountability.

4.2 Example KPIs (Illustrative)

The following are examples only—final metrics should be developed collaboratively

between Council and DDA:

Section 5: Citizen Communications

Effective communication is essential for democratic governance. The population varies

greatly, and the part time residents do represent a substantial aspect of revenue. Given

Harbor Springs’ small full time population, and engaged part time population, achieving high

coverage is feasible at relatively low cost.

5.1 Current Challenges

• Audio/visual reliability issues noted during Council meetings

• No comprehensive email/text notification system for budget hearings or major

decisions

• Seasonal residents may miss important information

5.2 Suggestions

The budget includes $60,000 for A/V upgrades. Consider whether a portion of this could

fund active engagement systems:

1. Notification Platform: A mass notification system (email/SMS) capable of reaching

residents and property owners for major announcements

2. Contact Collection: Make email/phone collection a standard part of utility account

management and permitting

3. Coverage Target: Consider setting a goal to have 90% of utility accounts with valid

contact information within 2-3 years. Current technology may be sufficient, so a

coverage taget may be the missing element to an effective communications strategy.

4. Major Initiative Commitment: For significant decisions (budget, rate changes,

zoning), commit to direct mailing plus electronic notification plus clear website

postings

5. Measure: Use Net Promoter scoring to validate outcomes of communications

engagement. All KPIs for communications should be based on results not effort

Page 6 of 7City of Harbor Springs — FY2026 Budget Analysis

Section 6: Summary of Suggestions

The following suggestions are offered for Council’s consideration, grounded in GAAP and

GFOA best practices. Staff may have already addressed some of these points, and I

welcome correction where I have misunderstood.

Budget Adoption Considerations

1. Remove $500,000 boardwalk expenditure per staff recommendation; keep in CIP as

contingent

2. 3. 4. 5. Consider presenting a base budget that balances without $400,000 FEMA revenue

Adopt tiered CIP: Tier 1 (funded) and Tier 2 (contingent on external revenue)

If FEMA is received, consider prioritizing reserve replenishment before new projects

Request DDA propose KPIs and baseline performance estimate before budget

approval

Near-Term Process Improvements

6. 7. 8. 9. Calculate and disclose total PTO liability; consider establishing benefit reserve fund

Complete 10-year Electric Fund pro forma before finalizing bond decisions

Consider quarterly utility reporting to Council

Formalize Electric Fund transfer policy with coverage safeguards

10. Publish CIP on website with funding status clearly labeled

11. Launch citizen notification enrollment campaign

Strategic Guidance

• Consider providing explicit Council guidance on CIP priorities (resident infrastructure

vs. tourism amenities)

• Clarify DDA mission expectations: business development vs. placemaking vs. capital

improvements

• Consider engaging informal utility advisory input before major bond decisions

Harbor Springs is a small city with sophisticated responsibilities: a municipal electric utility,

an active DDA, waterfront facilities, and a capital plan that would not be out of place in a

larger community. These suggestions are intended to help align the budget more closely

with GAAP best practices and strengthen transparency for the 1,200 year-round residents

who depend on these decisions.

Again, I had limited time to review these materials and may have missed important context. I

welcome correction on any point and appreciate the substantial work that staff and Council

invest in the City’s governance.

Thank you for considering these observations.

Carter Williams

355 East Bay Sreet

Harbor Springs, MI 49740

Page 7 of 7

Common ways cities handle longer submissions

Many councils use one of these approaches:

A. Page limit for the main packet, with attachments allowed

Example:

-

1–2 page letter in the agenda packet

-

Full 7-page analysis included as an attachment or appendix

-

Or posted online as “Correspondence Received”

B. Summary + full document on file

-

Council receives a summary

-

Clerk keeps the full analysis on record

-

Full version is public and FOIA-able

C. No formal limit, but discretion by staff

-

Clerk decides what goes into the packet

-

Everything is still “received,” even if not printed in full

4. What cannot happen

Even if the city limits packet length:

-

❌ They cannot refuse to accept your letter

-

❌ They cannot discard or ignore it

-

❌ They cannot prevent Council from receiving it

-

❌ They cannot block it from the public record

If submitted on time, it is public correspondence.